Submitted by Jeffrey Snider – Alhambra Investment Partners

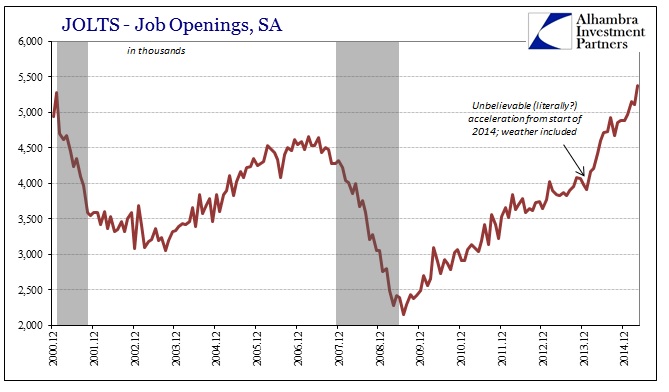

The latest updates for the JOLTS showed that job openings in April surged to a new series high. Jumping by 267k (seasonally adjusted), the trend in job openings is being used as confirmation that there must be some robust underlying trend in overall payrolls despite the ubiquitous slump everywhere else. In other words, this is another series from the BLS that appears to be confirming the Establishment Survey’s view on the economic pickup.

“This is more confirmation that the economy is indeed emerging from that soft patch in the first quarter and can still pick up even faster in the next few months,” said Chris Rupkey, chief financial economist at MUFG Union Bank in New York.

Job openings, a measure of labor demand, rose 5.2 percent to a seasonally adjusted 5.4 million in April, the highest level since the series began in December 2000, the Labor Department said in its monthly Job Openings and Labor Turnover Survey (JOLTS).

Ever since the start of 2014, weather be damned, the pace of job openings has simply decoupled from all perception except the Establishment Survey. While that offers “more confirmation” for economists, in reality it amounts to the same confirmation. The JOLTS survey is benchmarked to the BLS’s Current Employment Situation (CES), meaning that if there is a trend-cycle problem in the mainline payroll report it will passed along, directly, to JOLTS.

From the BLS itself:

JOLTS total employment estimates are benchmarked, or ratio adjusted, monthly to the strike-adjusted employment estimates of the CES survey. A ratio of CES to JOLTS employment is used to adjust the levels for all other JOLTS data elements.

Given that baseline, it would be highly suspect and relevant only where the JOLTS figures diverge from the Establishment Survey. While none of the components had done so for most of 2014, that isn’t the case more recently. While Job Openings have supposedly surged, the hiring rate has not. Dating back to last October, hiring appears to have frozen if not slightly declined. Continue reading

The use of propaganda to further geopolitical and socioeconomic objectives are complex methods of positioning arguments and manufacturing preconditioned counter arguments. This ‘seeding of the field beforehand’ has become commonplace, predictable, and can be trended with relative ease.

The use of propaganda to further geopolitical and socioeconomic objectives are complex methods of positioning arguments and manufacturing preconditioned counter arguments. This ‘seeding of the field beforehand’ has become commonplace, predictable, and can be trended with relative ease.

Row, row, row your boat …

Row, row, row your boat …

You must be logged in to post a comment.