Submitted by Dr. Paul Craig Roberts – Institute for Public Economy

There are no free financial markets in America, or for that matter anywhere in the Western word, and few, if any, free markets of any other kind. The financial markets are rigged by the big banks, the Federal Reserve, and the Treasury in the interests of the profits of the few big banks and the dollar’s exchange value, which is the basis of US power.

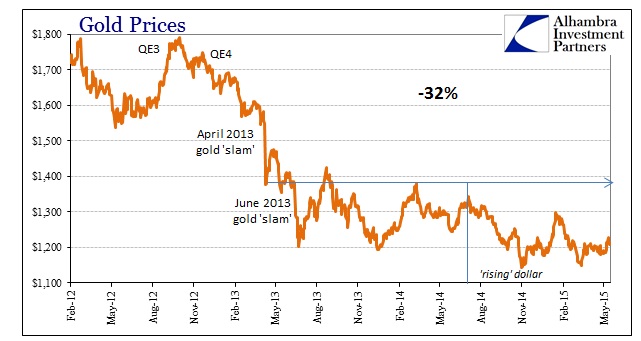

There is a contradiction between a strong currency on one hand and on the other hand massive money creation in order to sustain zero and negative interest rates on the massive debt levels. This inconsistency is revealed by rising gold and silver prices.

When gold hit $1,900 an ounce in 2011 the Federal Reserve realized that the precious metal market was going to limit its ability to provide enough liquidity to keep the thoughtlessly deregulated financial system afloat. The rapid deterioration of the dollar in terms of gold and silver would sooner or later spill over into the exchange value of the dollar in currency markets. Something had to be done to drive down and to cap the gold price.

The Fed’s solution was to take advantage of the fact that the prices of gold and silver are determined in the futures market where paper contracts representing gold and silver are traded, and not in markets where the physical metal is actually purchased by people who take possession of it. The Fed realized that uncovered short sales provided enormous leverage over the prices of the metals and that it would be profitable for the bullion banks, such as JPMorgan, Scotia, and HSBC, to short the market heavily and then cover their shorts at lower prices produced by selling as a result of triggering stop-loss orders and margin calls.

Dave Kranzler and I have shown on numerous occasions that the bullion banks and the Federal Reserve make profits and protect the dollar by suppressing the prices of gold and silver. They do this by illegally selling huge numbers of uncovered shorts in the futures market. This illegal operation is supported by the so-called “regulatory authorities” who steadfastly refuse to intervene.

It has just happened again. Dave Kranzler describes it in detail here:http://investmentresearchdynamics.com/bullish-news-for-precious-metals-and-goldsilver-get-paper-smashed/

If memory serves, Matt Taibbi explained a few years ago how Goldman Sachs got position limits removed from speculators, so that now speculators can dominate market forces.

Neoliberal economists in service to the financial sector have created a rationale for why interest rates can be negative in the face of massive debt and money creation and a slew of troubled financial instruments from corporate junk bonds to sovereign debt. The rational is that there is too much saving: The excess of savings over investment forces down interest rates. The negative interest rates will discourage people from saving and encourage them to spend, because the price of consumption in terms of foregone future income from saving is zero. It even pays to consume, because saving costs more than it earns. Continue reading

Viktor Orban, wearing his Brussels frown

Viktor Orban, wearing his Brussels frown

You must be logged in to post a comment.